Controlling Costs of a Patent Portfolio: The Little Things Do Matter

As former in-house IP counsel, as well as through our work with some of the top university tech transfer offices (TTOs) and corporate patent departments in the country, we’ve seen many good (and some not so good) processes for IP management. In this article, the second in a series of posts focused on common problems in patent portfolio management, we will discuss the importance of managing patent-related costs and will provide recommendations on how to improve cost efficiency.

As former in-house IP counsel, as well as through our work with some of the top university tech transfer offices (TTOs) and corporate patent departments in the country, we’ve seen many good (and some not so good) processes for IP management. In this article, the second in a series of posts focused on common problems in patent portfolio management, we will discuss the importance of managing patent-related costs and will provide recommendations on how to improve cost efficiency.

It is usually easier to notice overspending in a budget than to pinpoint why it’s happening and how to fix it. Why? Because costs are often driven by an accumulation of little decisions that appear reasonable in isolation. For example, it may seem reasonable to pay a fee for an extension of time to file a response, if the extension provides useful time to address an issue or to make a decision, since the cost of doing so is relatively low. However, when such decisions become common practice, and are repeated across multiple applications, the aggregate costs can significantly impact annual budget and cash flow. In other words, a simple question (i.e., can we afford this extension fee?) can become a significant business process issue. We recommend that organizations practice good “hygiene” by managing the little things before they become bigger problems impacting the bottom line. Here are some tips on how to do this:

1. Track and Analyze Data.

Following the adage, you can’t manage what you can’t measure, you need to have a good system in place for tracking data associated with steps in the patent process. For example, to track extensions of time, an accounting system should track extension fees separately from all other fees; alternatively, a docketing system can track filing dates of responses. Ideally, data is tracked so that each cost occurrence is associated with an individual activity, thereby enabling all activities involving such costs to be identified and analyzed both individually and in the aggregate. Depending on your current systems, you may need to add data fields to a database or be creative with the data you do have, and to establish processes for data entry and analysis. In some cases, a portfolio review can identify specific process issues to target.

2. Consider the aggregate impact of actions across a portfolio on the annual budget.

While a single action affects the cost of only a single application, that kind of action, when repeated across several applications, impacts the annual budget. Put simply, if every application included an additional cost of $500 in a given year, then, in a large portfolio of 100 applications, that cost requires $50,000 in the annual budget.

Now, consider a more complex example. In year one, you file 10 new patent applications. In the following year, you file PCT applications for them, as well as another 10 new patent applications. In year three, you file 10 new patent applications, 10 new PCT applications, and 15 new national phase applications (say, 5 applications in 3 countries each). As the portfolio grows, the required annual budget and flow of documents also increases. Generally, growth will continue for about 10 years before leveling off, with an annual budget around 5 to 10 times the budget of year one.

Of course, the significance of an aggregated cost depends on the anticipated size of the portfolio. A small fee of $75 may be relatively insignificant when incurred across a portfolio of ten, compared to a portfolio of one hundred. To help make these decisions, we advise clients to create a financial model of expected portfolio growth when preparing to discuss budgets.

3. Track “time to disposition” and its related cost.

Time to disposition is the time between filing an application and disposition of that application through grant, abandonment or expiration. While applications are pending, there is typically one interaction, at a minimum, with the Patent Office each year, resulting in an annual expense for each application. Likewise, there are annual costs associated with granted patents. By reducing time to disposition, either by bringing applications to closure through abandonment or grant, or by allowing granted patents to expire, total annual costs for the portfolio are also reduced.

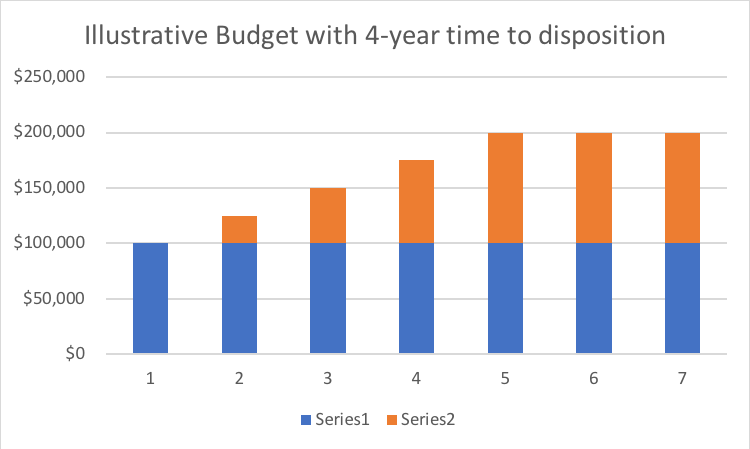

For example, assume that 10 new patent applications are filed per year, and each pending application costs about $2500 per year. The graphs below show the annual budgets for new (series 1) and pending (series 2) applications over a period of seven years, with average time to dispositions of 4 years and 5 years, respectively. By reducing average time to disposition from 5 years to 4 years, the annual budget for the pending applications is reduced by about 20% (In this example, $25,000 per year). Time to disposition is also a significant factor in controlling both the time and the level at which an annual budget’s growth levels off. Data tracking this measure, along with guidelines and processes for addressing it, are helpful tools for controlling the budget.

4. Know the Patent Office fee schedules.

As most are aware, the U.S. Patent Office charges fees for each independent claim over three, and for each claim over a total of twenty. For instance, if you have six independent claims and forty total claims, the additional charges will total $1690.00 (based on the current fee schedule), which can be significant for a small entity. The same is true in foreign jurisdictions. The European Patent Office charges €235 per claim over 15 claims, and China’s Patent Office charges for each claim over 10 claims. Many patent offices have other ancillary fees, such as for late filings, exceeding page count limits (e.g., PCT filings with more than 30 pages), extensions of time, corrections of errors, and the like. For a sizable portfolio, these fees in the aggregate can take a toll on the annual budget.

5. Act earlier.

An organization may choose to delay taking an action in order to defer costs. However, delays can actually increase costs. For instance, filing for an extension of time not only increases average fees incurred per application, but also extends the average time to disposition. As another example, an applicant may submit to the U.S. Patent Office an “information disclosure statement” (IDS) citing prior art for consideration. If the Patent Office happens to issue an office action or a notice of allowance before an IDS is filed, the submission of the IDS will now be subject to additional fees and/or papers to be filed. In yet another example, delays may make it more difficult (requiring more time and thus more money) to obtain cooperation from inventors and other participants in the process with such basic tasks as obtaining signatures. Therefore, the number and timing of actions must be part of the equation in managing costs. Having well-established guidelines and processes also helps in this regard.

6. Act less often.

Each time an action is taken with respect to a patent or pending patent application, some cost is incurred. Whether the action is taken by a Patent Office, the applicant’s legal representative, or the applicant itself, the time and effort spent processing communications to and from patent offices and between applicants and their legal representatives triggers a cost. A simple example is the difference between filing a complete patent application and an incomplete one, with the latter requiring nearly twice as many communications among the involved parties. Essentially, productivity goes up and costs come down by simply taking fewer actions. Again, well-established guidelines and processes are essential to any effort to manage costs.

7. Establish guidelines, processes, and tools to manage costs.

To control a specific cost, everyone whose actions impact that cost must be on the same page. This consistency is best achieved by establishing guidelines for internal staff, inventors, and outside counsel which both set and communicate expectations. In addition, appropriate processes and controls, that work for all involved, should also be developed to implement guidelines in the day-to-day operations. Tools supporting these processes, as well as those which track and analyze data, are the remaining pieces of the puzzle. Working together, guidelines, processes and tools can help reduce costs, identify cost drivers, and estimate and communicate annual budgets.

As a patent portfolio grows, so too does the need to control costs. After all, the cost savings may be the difference between a few more patents in the portfolio or even a few more personnel in the office.

Patent GC routinely works with TTOs and corporations to help improve their internal patent processes and promote sound cost management. We provide our clients with recommendations tailored to their own day-to-day operations, including clearly defined responsibilities for all stakeholders in the patent process, checklists and a docketing system designed to implement new processes, and periodic portfolio reviews to detect potential issues and ensure compliance.

If you have questions about how to improve internal processes for patent portfolio management, our team would be happy to help. Feel free to contact Peter Gordon directly at pgordon@patentgc.com or to request more information by visiting our Contact Us page.